The Indian Rupee (INR) is trading positively against the US Dollar (USD) on Tuesday after a three-day losing streak. The USD/INR pair is correcting to near 90.35 as the US Dollar Index (DXY) fell sharply after hitting a new low in more than three weeks at 98.86 on Monday. The US dollar came under pressure as risk aversion sentiment declined, leading to a decline in demand for safe haven assets.

The US dollar rose sharply on Monday as market sentiment turned risk-off, following the US strike on Venezuela and the arrest of President Nicolas Maduro over drug trafficking charges.

Meanwhile, the outlook for the Indian rupee remains fragile due to renewed trade frictions between the US and India, and the continued inflow of foreign funds from the Indian stock market.

On Monday, US President Donald Trump threatened to increase tariffs on India if it continues to buy oil from Russia. “We can raise tariffs on India if they don’t have help on the Russian oil issue,” Trump said.

On the foreign inflows front, foreign investors continue to shed their stake in the Indian stock market. Foreign Institutional Investors (FIIs) offloaded their stake worth Rs. 3,015.05 crore in the first three trading days of January. However, the amount of shares sold on Monday was worth Rs. 36.25 crores, much lower than the average sale.

Daily summary of market drivers: Investors shift their focus to US non-farm payrolls data

- The sharp decline in the US dollar was also driven by surprisingly weak US December manufacturing Purchasing Managers’ Index (PMI) data on Monday.

- The data showed that the manufacturing PMI contracted again at a faster pace to 47.9 from 48.2 in November. Economists expect the data to come in slightly higher at 48.3. The data also showed that subcomponents of the manufacturing sector, such as the new orders index and employment, also declined, but at a moderate pace.

- The continued decline in manufacturing sector activity has raised concerns about the US economic outlook.

- This week, the main catalyst for the US dollar will be the non-farm payrolls (NFP) data for December, which will be published on Friday.

- Investors will pay close attention to official US employment data for new signals about the current state of the labor market. In 2025, the Federal Reserve (Fed) makes three interest rate cuts and pushes them down to 3.50%-3.75% to support weak labor market conditions.

- This year, UBS expects the Fed to cut interest rates in July and October. Investment banking to financial services-led firms pushed forward expectations from January and September, indicating that the core Consumer Price Index (CPI) could rise by 44 basis points, 50 basis points, and 30 basis points in December, January, and February, respectively.

- On Wednesday, investors will closely monitor ADP employment change data, ISM services PMI data for December, and JOLTS job openings data for November.

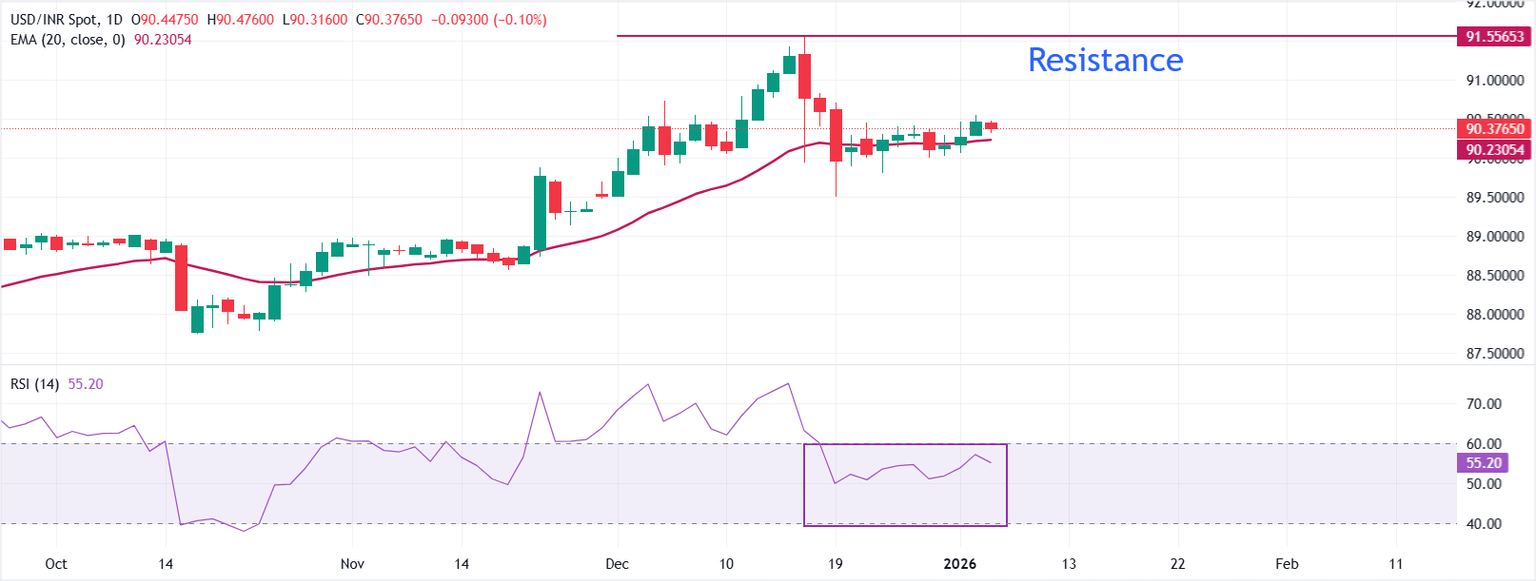

Technical Analysis: The USD/INR pair is having difficulty breaching the 90.50 level

On the daily chart, the USD/INR pair is trading at 90.3765. The pair is holding above the bullish 20-day exponential moving average (EMA) at 90.2305, which supports the broader uptrend after the recent pullback. The slope of the average has flattened, yet price action continues to respect it as dynamic support.

The 14-day Relative Strength Index (RSI) at 55.20 (neutral) indicates steady momentum without overbought pressure, keeping the near-term bias somewhat positive.

Momentum will improve on a sustained close above the short-term average which could create the opportunity for the pair to revisit its all-time high at 91.55. Conversely, a daily close below the 20-day EMA would shift the bias lower and open room for further bounce towards the December low at 89.50.

(The technical analysis for this story was written with the help of an artificial intelligence tool.)

Frequently asked questions about Indian economy

The Indian economy has averaged a growth rate of 6.13% between 2006 and 2023, making it one of the fastest growing economies in the world. India’s high growth has attracted a lot of foreign investment. This includes foreign direct investment (FDI) in physical projects and foreign indirect investment (FII) by foreign funds in Indian financial markets. The higher the investment level, the greater the demand for the rupee (INR). Fluctuations in dollar demand from Indian importers also affect the Indian rupee.

India has to import a significant amount of its oil and gasoline needs, so the oil price can have a direct impact on the rupee. Oil is mostly traded in US dollars (USD) in international markets, so if the price of oil rises, the overall demand for USD increases and Indian importers have to sell more rupees to meet this demand, which leads to a depreciation of the rupee.

Inflation has a complex impact on the rupee. It ultimately indicates an increase in money supply which reduces the overall value of the rupee. However, if the interest rate rises above the RBI’s target level of 4%, the bank will raise interest rates to bring it down by reducing credit. Rising interest rates, especially real rates (the difference between interest rates and inflation) boost the rupee. It makes India a more profitable place for international investors to put their money. Lower inflation could be supportive for the rupee. Meanwhile, low interest rates could have a negative impact on the rupee.

India has run a trade deficit for most of its modern history, suggesting that its imports exceed its exports. Since the majority of international trade is conducted in US dollars, there are times – due to seasonal demand or abundant demand – when a high volume of imports creates a large demand for US dollars. During these periods the rupee can weaken as it is sold heavily to meet the demand for dollars. When markets witness increased volatility, demand for the US dollar can also rise with a corresponding negative impact on the rupee.